When it comes to choosing a Medicare Advantage plan, there are a lot of things to consider. How much will it cost? What kind of coverage do I need? What kind of provider networks are available in my area? Thankfully, there is help available to make the process easier.

The Medicare.gov Plan Finder tool is the most effective approach to compare all of your area’s Medicare Advantage options. Medicare Advantage plans provide medical and usually Part D drug insurance from a private insurer.

Whether you’re new to Medicare or looking to switch plans, it can be tough to figure out which Medicare Advantage Plan is right for you. Luckily, we’re here to help! In this post, we’ll outline the basics of Medicare Advantage Plans and walk you through how to choose the best one for your needs. So sit back and relax – we’ve got this!

Are Medicare Advantage Plans Good or Bad?

Now before I start there’s something I want to say. You’ll see a lot of videos on the internet talking bad about Medicare Advantage. While Medicare Advantage has many disadvantages it also has many positives. I have clients on Medicare Advantage plans that are perfectly happy. I also have clients on Medicare Supplements and they are happy too.

What is the Goal of Independent Broker?

My goal is to present the facts to allow you to make the best decision for what your needs are. Many times I have husbands and wives on different programs with different companies. The reason being Medicare is not one size fits all. That’s why there are many options. It’s because of these options Medicare can become very confusing. It’s my job to answer all of your questions and help you pick the exact right plan for your needs.

“Chris, what is better, Medicare Advantage Plan or Original Medicare with a Medicare Supplement?”

My answer is, let me present you the facts. Then you will ask me questions and it will become very clear what is best for you. What is exactly right for you is probably not exactly right for your neighbor, or family member, etc. We want you to get what is right for you.

What is Medicare Advantage Plan?

Ok, let’s get to why you’re here. The first question to answer is What is a Medicare Advantage plan? I take this right from Medicare’s website because I think it answers the question best. It states, “Medicare Advantage Plans, sometimes called “Part C” or “MA Plans,” are an “all in one” alternative to Original Medicare. They are offered by private companies approved by Medicare. If you join a Medicare Advantage Plan, you still have Medicare.

These “bundled” plans include Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance), and usually Medicare drug coverage (Part D).” I would like you to pay particular attention to the sentence, “If you join a Medicare Advantage Plan, you still have Medicare.” You might be asking, “Why are they telling me if I get a Medicare Advantage plan I still have Medicare, why wouldn’t I have Medicare if I get a Medicare Advantage Plan?”

Medicare Advantage Plan is a Replacement for Original Medicare

- The reason they say “you still have Medicare” is if you elect to get a Medicare Advantage Plan. It’s literally a replacement for Original Medicare.

- Medicare Part A, hospital insurance, and Medicare Part B medical insurance is also called Original Medicare. Original Medicare is a very important term to know. When you have Original Medicare the federal government is your primary insurance. They make the decisions on what is covered and not covered etc.

- Getting back to Medicare’s definition of Medicare Advantage. They state that Medicare Advantage Plans “are offered by private companies approved by Medicare.” This means, if you elect to get a Medicare Advantage Plan. Your primary Medicare coverage will be coming from the private insurance company. Not the government or not directly from Medicare.

- You still have Medicare, but your coverage will be coming from the private Medicare Advantage company and not Original Medicare. These are the basics about Medicare Advantage. When you start to understand the basics you get to make a well-informed decision on what is best for you.

What are the Benefits of Having Medicare Advantage?

This is where some of you will really make your decision if Medicare Advantage is right for you. I like to start with the positives, here are the positives in my opinion.

- The first positive is many Medicare Advantage plans have low to $0 monthly premiums. There are some that will actually reduce your Part B premium for having their plan. One thing I need to cover is you always must pay your Part B premium to Medicare. I get asked many times by new Medicare Beneficiaries, “if I get a Medicare Advantage plan or a Medicare Supplement plan do I still have to pay for Part B of Medicare?” The answer is absolutely yes. We know Uncle Sam isn’t going to miss out on getting money.

- Many Medicare Advantage plans, as I said, have a $0 to low monthly premium. Many also cover Part D prescription coverage as well. It’s these low costs that make Medicare Advantage a very desirable option for many. These low costs lead the way on why some of my clients decide to have Medicare Advantage.

Medicare Advantage Plan can offer additional coverage like Dental, Vision, and Hearing

- In addition, Medicare’s website states, “Most Medicare Advantage Plans offer coverage for things Original Medicare doesn’t cover, like some vision, hearing, dental, and fitness programs (like gym memberships or discounts). Plans can also choose to cover even more benefits. For example, some plans may offer coverage for services like transportation to doctor visits, over-the-counter drugs, and services that promote your health and wellness.

- Plans can also tailor their benefit packages to offer these benefits to certain chronically ill enrollees. These packages will provide benefits customized to treat specific conditions.”

How can Medicare Advantage Plans be Free?

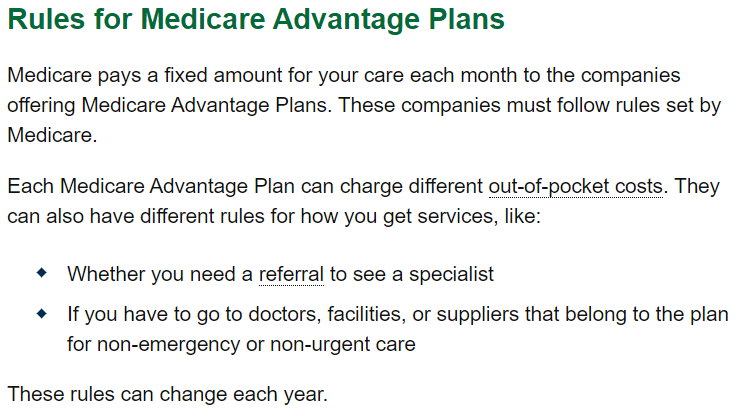

Another question I get asked about Medicare Advantage is, “how can these plans be free or how can they pay me for being on their plan?” Remember when I outlined that Medicare stated that if you have a Medicare Advantage Plan you still have Medicare, but you get it from the private insurance company. What this means is, and I take this right from Medicare’s website too. It states, “Medicare pays a fixed amount for your care each month to the companies offering Medicare Advantage Plans.” What happens is that instead of Medicare paying your medical bills directly, Medicare pays a monthly premium to the Medicare Advantage company you pick, instead of paying your medical bills directly.

Out of Pocket Maximums Original Medicare doesn’t Have

- Another positive is Medicare Advantage Plans have is maximum out of pocket. Having Original Medicare only doesn’t have a maximum out of pocket.

- Medicare Advantage plans are basically pay-as-you-go plans.

- You make a copayment for each service you get:

- You may have a copayment to see a primary care physician or a specialist

- a copay for being an in-patient in the hospital

- a copay for an MRI or x-ray

What is the Maximum Out-of-pocket for Medicare Advantage Plans in 2021?

There are many of these copays. But these Medicare Advantage plans have a maximum out-of-pocket you are responsible for. This max out of pocket is for services that would fall under Part A and Part B claims. The highest out-of-pocket max in 2021 a Medicare Advantage Plan can have is $7,550 for in-network services. The highest for out-of-network services in 2021 is $10,000. More on in and out of network services in a minute. The numbers I just mentioned are the maximum set by Medicare. Each plan may have different max out of pockets, but the highest they can set are these numbers. I have some clients that are on Medicare Advantage Plans with max out of pockets as low as $999 for in-network services. Each plan can be different. That is one of the things I believe someone considering Medicare Advantage should look at closely.

Why is an Insurance Agent Important?

Being independent allows me to present each plan’s coverage and options objectively. When you call a Medicare Advantage company directly. They will only be able to tell you about their plan and cannot compare all of the companies. You can decide what type of objectivity you would get when calling a company directly. But with me, I’m here to listen to what your needs are. I look at everything available and get what is in your best interest. Call or email me for help. Here’s the number to call 800-910-3382.

To sum up what I think the positives to Medicare Advantage Plan are:

1) Low to $0 dollar monthly premiums and some can reduce the Part B premium you pay the government.

2) Medicare Advantage covers everything Original Medicare covers. In addition, plans can cover things that Original Medicare doesn’t cover like, some dental, vision hearing needs. Transportation to doctor visits, some cover gym memberships, over-the-counter pharmacy benefits, and more. To give an example of how far these benefits can go. I represent a plan that actually will pay up to a certain amount to have your pet boarded. In case of a hospital or skilled nursing stay.

3) Most have Part D prescription coverage included.

Disadvantages of Medicare Advantage Plan

Now that takes us to the disadvantages.

The main disadvantage I see with Medicare Advantage Part C is the restrictive doctor networks. My clients tell me is the number one reason they don’t have or want a Medicare Advantage Plan. Is the potential of a very restrictive doctor network. Most Medicare Advantage Plans operate within an HMO system. If you don’t know, that stands for Health Maintenance Organization. This means there is a network of primary care physicians, specialist physicians, hospitals, durable medical equipment providers, etc. If you see a provider outside of this network you don’t have any coverage. Unless you are having an emergency. Emergencies are always covered anywhere in the United States and some Medicare Advantage Plans have worldwide emergency coverage.

If you see a provider outside of the network you will be responsible to pay 100% of the bill. If you need to see a specialist with an HMO plan. You need a referral from your primary care physician first. In fairness to Medicare Advantage HMO plans. Some have added a benefit in them that allows you to self refer to in-network specialists. Although there are not many of these plans, they are available in some areas. When I explain how an HMO network can be restrictive on the doctors. My client’s focus shifts to keeping Original Medicare and purchasing a Medicare Supplement to cover the gaps of Medicare.

HMO Medicare Advantage Plan Provider Networks can change at any Time

Another disadvantage of the Medicare Advantage Plans is the network of doctors can change at any time. When you enroll, your doctor may be in the network. However, a doctor or plan may decide not to contract together any longer at any time. This wouldn’t be a big deal if you could simply change to a different Medicare Advantage Plan anytime during the year. Or simply return to Original Medicare, but you can’t. The time frames to make elections in and out of Medicare Advantage are very restrictive as well.

What is the Benefit of a PPO?

I said I would touch on HMO and PPO Medicare Advantage Plans. I described the HMO, so let me briefly describe the PPO plan. PPO stands for Preferred Provider Organization. When you have a Medicare Advantage PPO plan, this means there are in-network providers. Those that have already agreed to take the plan, and providers that are out of network. Basically, the in-network providers have already agreed to terms and payments from the plan. Any provider that isn’t in-network, hasn’t agreed to the terms and payments. If you have a Medicare Advantage PPO plan you know you will have coverage for any in-network providers.

In general, the list of PPO in-network providers is larger than an HMO network. With a PPO Medicare Advantage plan, you can also have coverage potentially to any provider that is not inside of the PPO network. It’s really like a hybrid plan. However, you need to be careful when you are being educated about these programs from unskilled agents. They will often tell you, you don’t have to worry about networks with a PPO plan. Because this plan has in-network and out-of-network coverage. Now, you may have coverage, but the provider you see may not accept the plan for payment. Leaving you to file claims with your Medicare Advantage plan.

More on Medicare Advantage Plan Disadvantage

- The last disadvantage I’ll talk about is each Medicare Advantage Plan can charge different out-of-pocket costs.

- Each plan can and does have different copays for services. For example:

- They may have a $0 primary care physician office visit copay and some may charge $20 or more

- r may not have a copay to be an inpatient in the hospital

- some may charge $500 a day or more for a certain amount of days in the hospital The copays can vary greatly from plan to plan and the copays can change every year.

What to Know About Medicare Advantage Plans and Original Medicare?

I am going to get on my soapbox here for a moment and I’ll keep it brief. In my opinion, it’s important to talk with an independent agent that believes in both Medicare Advantage and Original Medicare with a Medicare Supplement. I have many people across the country that find my blogs and videos on Youtube and they have signed up for a Medicare Advantage or Medicare Supplement through an agent without knowing both exist.

- The television commercials with celebrities like football hall of farmers and actors are trying to get you to call in and the people on the other side of the phone want you to get a Medicare Advantage Plan

- They will likely only tell you the positives without outlining the negatives

- Many times agents that you contact are employed by a company that only represent one type of plan or company. And simply won’t tell you about the other options

Avoid Medicare Plan Agents that Don’t Believe in Medicare Advantage or Medicare Supplements

Many times there are agents that simply “don’t believe” in Medicare Advantage or they “don’t believe” in Medicare Supplement and won’t offer both options. They won’t even talk about it. Additionally, agents that just offer one or the other just don’t want to do the work to become experts in both. And usually, the agents that “don’t believe” in a particular program, “don’t believe” in Medicare Advantage. Again, in my opinion, it is easiest not to “believe” in Medicare Advantage, because it is a lot more complicated than Original Medicare with everything it can offer. Furthermore, because Medicare Advantage has all of these extra options, the number of training agents must do every year to stay certified to provide Medicare Advantage Part C can be very difficult, extremely time-consuming, and expensive.

Instead of doing the necessary certification every year, they may say something like, “oh Medicare Advantage, it is very restrictive you don’t want it.” I choose to learn and spend the extra time and money to certify to provide Medicare Advantage so you get the full story. And if you have read my other blogs watched my Youtube videos, I always say I am here to present all of your options to help you make the exact right decision for your exact needs. I don’t advocate for one or the other, I just want you to get what is best for you. And I hope you use me to get it. Ok, thanks for sticking with me through that.

How Do I Get a Medicare Book?

If you want to learn more I suggest a couple of Medicare publications. 1st is the Medicare and you Handbook Medicare puts out every year. And also Medicare’s official guide called Understanding Medicare Advantage Plans. Depending on where you are reading this there will be a link somewhere to download your own copies if you don’t already have them. This went longer than I wanted, thank you for reading all the way through, but I feel what I covered is very important to help you to decide if Medicare Advantage is right for you.

Key Takeaways

Medicare Advantage Plan positives:

- $0 to low monthly premiums. Usually have Part D Prescription coverage.

- Can cover extras Original Medicare doesn’t cover, dental, vision, hearing, fitness coverage, transportation to doctor visits, over-the-counter drugs, and others. They also have maximum out of pockets.

Medicare Advantage Plan disadvantages:

- Can have very restrictive doctor networks

- Unpredictable copays

- Doctor networks can change at any time

- Each plan can have different copays and they can change every year.

About The Author — Christopher Duncan

I’m Chris Duncan, owner of Trusted Benefits Direct. As your Medicare advisor, I want you to know that my business offers superior solutions for everyone. I do not work for insurance companies, which allows me to serve you at a high level without any hidden agendas or conflicts of interest. All resources are provided at no cost because people must find peace of mind when looking ahead years down the line.

As an insurance agent, it’s my goal to make your life easier. That includes the process of securing all types of coverage for you and your loved ones, including Medicare Supplements, Medicare Advantage, Medicare Part D, Final Expense life insurance services, and retirement security plans. You can reach me toll-free at 800-910-3382 or get a free quote on MedicareRateQuote.com with just a few clicks! Don’t forget that I also offer contact forms if you would like more information from trustedbenefitsdirect.com – click here now!

Important YouTube Channel Details

I appreciate you looking through my article. If it is interesting to you, please subscribe to my YouTube channel. Don’t forget to share this on social media channels such as Facebook and Twitter so your friends can read it too! I appreciate it when people take the time to comment or post their opinion of my articles to continue writing content related to Medicare basics, Medicaid Made Clear, Medicare Explained, Medicare 101, and others. It’s always nice to know that you’re reading my blog! Of course, I’m looking forward to seeing more of you soon on my next blog!