This article will focus on when Medicare Supplement plans pay claims for the gaps in Medicare. When seniors first start learning about Medicare they begin to realize where Medicare falls short. I have covered this in other videos and articles. But a quick example of a gap in Medicare is the Part A deductible. The Part A inpatient deductible is $1,408 in 2020 per benefit period. Part A has other costs you are responsible for. But for the sake of time will not go through them here.

Medicare Part B

The Part B deductible is $198 and after the deductible, there is 20% coinsurance. When seniors learn about the gaps and what they will be responsible to pay, their eyes turn to Medicare Supplements. It is the Medicare Supplements that help pay for the deductibles, coinsurance, and copayments Medicare doesn’t pay for. A quick example and this is not all-inclusive. Medicare Supplements will pay for things like the Part A deductible. Coinsurance for hospital stays lasting longer than 60 days. The Part B deductible and the 20% coinsurance the Medicare beneficiary is responsible for and more.

What are the Best Medicare Supplement Plans Companies

Clients regularly want to know which Medicare Supplement has a great reputation for paying claims. The answer I give is usually confusing to them. I tell them the Medicare Supplement company you choose. They make no decisions on when to pay a claim and when not to pay a claim. The reason it is confusing is that usually, they have had traditional non-Medicare health insurance for much of their lives. When a health insurance company covers you, I’ll use name brand examples, UnitedHealthcare, Aetna, Humana, Anthem, Blue Cross Blue Shield, and more when we have traditional health insurance. Our experience is with the health insurance company. It is the health insurance company that makes the decisions about what claims to pay, what claims you don’t pay. This is the relationship we are used to with our health insurance company.

How Original Medicare Works

What is covered and not covered is the decision of Original Medicare. I want you to notice I said Original Medicare. What I am talking about now has nothing to do with Medicare Advantage. If you have read my other articles. Or seen some of my other videos you know that Medicare Advantage is literally a replacement for Original Medicare. And as I always say, there isn’t anything wrong with Medicare Advantage. We have hundreds of clients with Medicare Advantage, but Medicare Advantage has some very different rules than Original Medicare. Medicare Advantage is more like traditional health insurance. The Medicare Advantage company makes more decisions on what is covered and not covered.

Original Medicare is the primary insurance. Original Medicare dictates what is covered, not covered, etc. A Medicare Supplement plan does not make any decisions and never influences Original Medicare’s decisions on claims. No matter what Medicare Supplement plan and company you choose, you will know they have nothing to do with the decision-making process of what claims are covered and what claims are not covered by Original Medicare.

Original Medicare and Medicare Supplement plans Example

Here is an example of a Medicare beneficiary having a heart attack and was 5 days. We will assume all treatments were Medicare-covered which is likely. Medicare is going to pay the entire Part A claim except for the Part A deductible which is $1,408 in 2020. So for a hospital stay of 60 days or less Medicare will pay all Medicare-covered claims, whether the claims are $2,000 or $100,000 or more. They will pay all Medicare-covered claims except the Part A deductible.

The Part A deductible of $1,408 is what the Medicare beneficiary would be responsible for. Now let’s say the Part B claim was $10,000 and I am just making up a number for math purposes. And we will say the Medicare beneficiary has not paid their Part B deductible of $198 for the calendar yet. They will be responsible to pay the $198 and 20% of the remaining $9,802. 20% of $9,802 is $1,960.40. That’s what they will be responsible for. Next, we will say the Medicare Beneficiary has a Medicare Supplement Plan G. And has not incurred any claims for the calendar year in which the hospital stay was incurred. Our fictional Medicare beneficiaries also enrolled in their Medicare Supplement plan when they first turned 65 and don’t have any pre-existing clauses. I will talk more about these pre-existing clauses more towards the end of the video.

What Medicare Pays

Medicare is going to pay the full Part A claim except for the $1,408 deductible. And Medicare will pay the full $10,000 Part B claim except for the $198 Part B deductible. Also, the remaining 20% coinsurance. To get the full amount the Medicare beneficiary will be responsible for in this example we need to add the $1,408 Part A deductible. The $198 Part B deductible and the 20% Part B coinsurance of $1960,40. You total all those together and the Medicare beneficiary will be responsible for $3,566.40 in this example. This is only an example for illustrative purposes and your costs can vary greatly.

Medicare Supplement Plans: Plan G

Plan G Medicare Supplement, as you probably know will pay all deductibles, coinsurance, copays, and any Medicare Excess charges, except for the Part B deductible. The Part B deductible in 2020 is $198. In this example I gave, the Medicare Beneficiary is going to be responsible to only pay the $198 Part B deductible. Because like I said when I laid out the example scenario, they had not paid their calendar year Part B deductible yet. If they had already paid their Part B deductible for the calendar year, then the Medicare beneficiary would not incur any out-of-pocket costs for this hospital stay.

Help Me Choose the Best Company

When I give this type of example to my new clients, they usually say something along the line of “Chris this sounds great, this is what I want. But how do I know the Medicare Supplement company I choose will pay these claims, and not deny them. I want to make sure I pick a company that has a great reputation for paying claims. I don’t want to be stuck paying these claims after I have paid all this money to the insurance company.” The answer to this is very simple and although Medicare can be very confusing. Medicare has gotten this portion right in my opinion in regard to how Medicare Supplements work with Original Medicare.

Because Original Medicare deemed these claims “Medicare Covered”, no matter what Medicare Supplement company the Medicare beneficiary has, that Medicare Supplement company must pay their portion of the claims as outlined in the benefits of the Medicare Supplement plan the Medicare beneficiary has chosen. Original Medicare truly dictates when Medicare Supplement companies pay and don’t pay claims. If Original Medicare approves a claim as Medicare Covered, the Medicare Supplement company must pay their portion as outlined in the benefits purchased. If Original Medicare deems a claim as not “Medicare Approved,” then Original Medicare will not pay the claims nor will the Medicare Supplement company pay any claims.

When Medicare Supplement Plans Can Deny Claims

Like I said before there are a few instances that the Medicare Supplement can deny to pay their portion on a Medicare Covered claim. I am going to explain these instances next. It is important to remember Medicare Supplement claim denials on Medicare Covered claims do not come up very often. Medicare Supplement plans have a right to deny their portion of a claim. If there is a pre-existing condition waiting period. There are only a select few times when a Medicare Supplement company may include a pre-existing condition clause. This is when a Medicare Supplement is purchased when medical underwriting is used. And the new policyholder did not have any creditable coverage before the purchase of their new Medicare Supplement policy.

Why Most People Don’t Have Pre-Existing Conditions Clauses

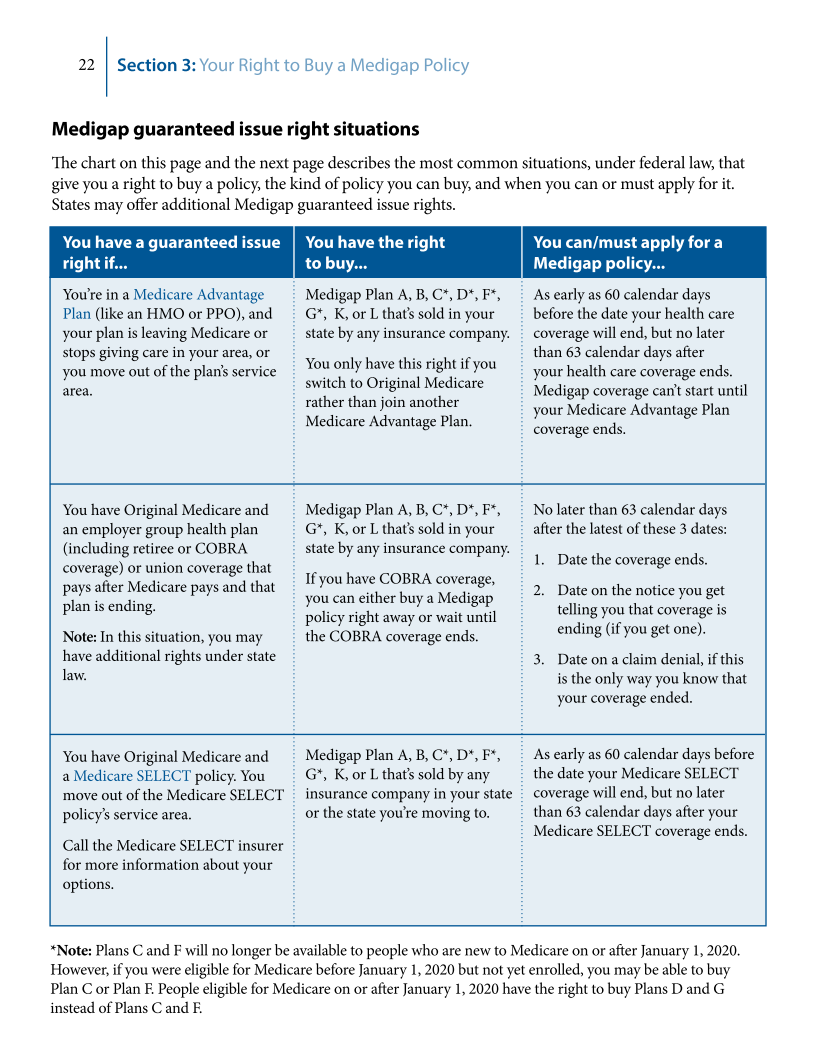

Most people purchase their Medicare Supplement during some type of open enrollment or guaranteed issue situation. A partial list of guaranteed issue or open enrollment situations for Medicare Supplements include loss of group coverage, turning 65, a Medicare Supplement is purchased with the first 6 months of Part B being effective, moving out of a service area of a Medicare Advantage plan, and many others as well. To view a full list of Medicare Supplement guaranteed issue rights, please open the official document from Medicare titled, 2020 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare and open to page 22 under the section Medigap guaranteed issue right situations.

When Medicare Supplements Have a Pre-Existing Waiting Period

A Medicare Supplement may have a pre-existing waiting period when a Medicare Supplement was purchased outside of a guarantee issue. Or open enrollment period. However, if a Medicare Supplement was purchased outside of this guaranteed issue or open enrollment period and there was prior creditable coverage and there was not a gap of creditable coverage of more than 63 days, then the new Medicare Supplement plan purchased MAY NOT invoke a pre-existing waiting period.

Examples of Creditable Coverage

If a Medicare Supplement was purchased outside of a guaranteed issue or open-enrollment time frame and the Medicare beneficiary had a prior Medicare Supplement they were replacing, this would be considered creditable coverage, and any pre-existing conditions would have to be covered from the first day of the new Medicare Supplement plan. For more information refer to page 15 of 2020 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.

Best Time to Buy A Medicare Supplement (Medigap) Policy

The Choosing a Medigap booklet states, “The best time to buy a Medigap policy is during your Medigap Open Enrollment Period.” This period lasts for 6 months and begins on the first day of the month. In which you’re both 65 or older and enrolled in Medicare Part B. Some states have additional Open Enrollment Periods including those for people under 65. During this period, an insurance company can’t use medical underwriting to decide whether to accept your application. This means the insurance company can’t do any of these because of your health problems:

- Refuse to sell you any Medigap policy it offers

- They will charge you more for a Medigap policy than they will charge someone who has no health problems.

- Make you wait for coverage to start (except as explained below)

While the insurance company can’t make you wait for your coverage to start, it may be able to make you wait for coverage related to a pre-existing condition. A pre-existing condition is a health problem you have before the date a new insurance policy starts. In some cases, the Medigap insurance company can refuse to cover your out-of-pocket costs for these pre-existing health problems for up to 6 months. This is what we call a ‘pre-existing condition waiting period.’ After 6 months, the Medigap policy will cover the pre-existing condition. Coverage for a pre-existing condition can only be excluded if the condition was treated or diagnosed within 6 months. Before the coverage starts under the Medigap policy. This is called the ‘look-back period.’ Remember, for Medicare‑covered services, Original Medicare will still cover any pre-existing conditions, even if the Medigap policy won’t, but you’re responsible for the Medicare coinsurance or copayment.”

Original Medicare Always Covers Pre-Existing Conditions

Something I want to interject here. For those that are new to Medicare and first learning the basic rules, it is easy to forget that your Medicare Supplement is secondary insurance. That is why, in my opinion, Medicare adds this last portion. And I’ll repeat it, says “Remember, for Medicare‑covered services, Original Medicare will still cover any pre-existing conditions, even if the Medigap policy won’t, but you’re responsible for the Medicare coinsurance or copayment.” Very rarely do we ever sell a Medicare Supplement to someone that will have a pre-existing waiting period?

Almost everyone I talk to comes to me either with some type of open enrollment or guarantee issue. Or I am changing their Medicare Supplement plan from one company to another company in order to save them money. And they had prior creditable coverage. When I do get a new client that comes to me and is buying a Medicare Supplement for the first time outside of open enrollment, guaranteed issue, or are buying the Medicare Supplement without prior creditable.

I fully explain this pre-existing condition waiting period for their new Medicare Supplement I make sure they understand that this waiting period is only for their out-of-pocket costs Medicare doesn’t pay. Original Medicare which is the primary never has any pre-existing condition waiting periods. If you think you will have a pre-existing clause on your Medicare Supplement, contact me toll-free at 800-910-3382. I will be able to ask you all the appropriate questions to find out for sure.

Conclusion

The gaps in Medicare are a reality for many seniors. As you get older, it’s important to keep up with the changes to your health plan and how these will affect you financially. In this article, I’ve covered one of the ways that senior citizens can protect themselves from financial burdens by understanding when their Medicare Supplement plans may pay claims. Did any of what I’ve shared today resonate with you? If so, please leave a comment below!

About The Author — Christopher Duncan

I’m Chris Duncan, owner of Trusted Benefits Direct. As your Medicare advisor, I want you to know that my business offers superior solutions for everyone. I do not work for insurance companies, which allows me to serve you at a high level without any hidden agendas or conflicts of interest. All resources are provided at no cost because people must find peace of mind when looking ahead years down the line.

As an insurance agent, it’s my goal to make your life easier. That includes the process of securing all types of coverage for you and your loved ones, including Medicare Supplements, Medicare Advantage, Medicare Part D, Final Expense life insurance services, and retirement security plans. You can reach me toll-free at 800-910-3382 or get a free quote on MedicareRateQuote.com with just a few clicks! Don’t forget that I also offer contact forms if you would like more information from trustedbenefitsdirect.com – click here now!

Important YouTube Channel Details

I appreciate you looking through my article. If it is interesting to you, please subscribe to my YouTube channel. Don’t forget to share this on social media channels such as Facebook and Twitter so your friends can read it too! I appreciate it when people take the time to comment or post their opinion of my articles to continue writing content related to Medicare Basics, Medicaid Made Clear, Medicare Explained, Medicare 101, and others. It’s always nice to know that you’re reading my blog! Of course, I’m looking forward to seeing more of you soon on my next blog!